Made in Europe or the Cracked shield.

What Better Than a Slogan to Re‑industrialise the Continent and Fend off Chinese Competition?

“EU Commissioner Stéphane Séjourné on Wednesday presented a strategy shutting Beijing out of EU public funding by introducing a European preference in strategic sectors. Countries which limit access to their own markets through local content rules would also be cut off.” (Euronews)

A picture is worth a thousand words, and L’Eclaireur is willing to bet that the introduction of European preference and the banning of China will result in the following plan :

What is the “Made in Europe” label really about?French Commissioner and Executive Vice-President of the European Commission Stéphane Séjourné announced a new tool to boost European industrialisation and counter Chinese competition. It sounds like a catchy slogan… and that’s pretty much all it is.The Industrial Accelerator Act (IAA) promises to protect European products and give them priority in public support schemes and public procurement. Beyond that? Little more than promises.

Because the European Union can do nothing more. The EU is a single market, and any measure that systematically favors “European” products could be deemed discriminatory—and thus contrary to the Treaty on the Functioning of the EU.

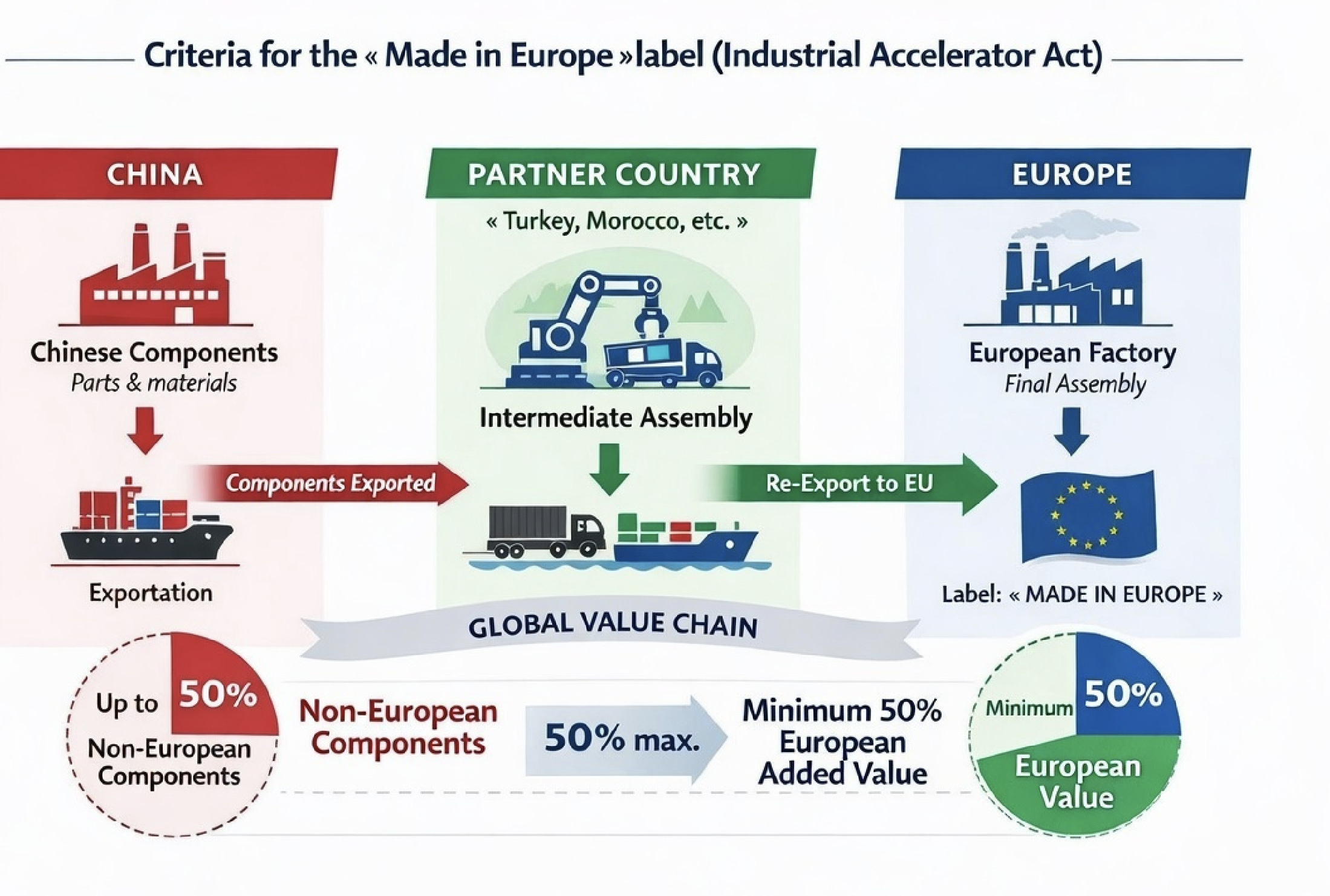

To comply with European laws and treaties, the IAA resorts to a series of contortions. Although the European regulation is still only a proposal—awaiting approval from both the European Parliament and the European Council—it already introduces substantial relaxations. Requirements have been eased on a case‑by‑case basis: country by country, sector by sector, and product by product. Moreover, public aid is now conditioned on a “simple” final assembly taking place in Europe.

Above all, the framework creates a hierarchy of “more‑ and less‑favoured” countries, with the better‑rated ones gaining greater access to European benefits. This circle of friendly nations is not limited to the 27 EU members; roughly 40 additional countries are vying for “Made‑in‑Europe” status to join the first tier of partners. These include—not only the United Kingdom, Norway, the United States, Japan, Canada, and Morocco—but also every nation that has signed a trade agreement with the European Union.

For all of these countries, the restrictions and added‑value thresholds have been loosened, resulting in what looks like a watered‑down form of European preference.

The European Commission has little room for manoeuvre—not only because of EU treaties but also due to the risk of a boomerang effect. Imposing too many barriers would inevitably sever the supply chains on which the bloc heavily depends and could trigger trade retaliation. A recent example is China’s pivotal role in the value chains of critical minerals and its April 2025 decision to introduce licensing agreements that allow the government to block the export of certain rare‑earth elements on a case‑by‑case basis.

Under the banner of a “European preference,” “Made‑in‑Europe” is likely to remain little more than a slogan—a purely bureaucratic exercise that will further burden a re‑industrialisation effort already struggling as energy prices soar. The goal is to raise industry’s share of European GDP from the current 14 % to 20 % by 2035—i.e., within less than a decade.

However, Europe’s industrial share of GDP has been falling for the past two‑to‑three decades—dropping from roughly 20–21 % in 2005 to about 14 % today. This decline stems from tertiarisation, offshoring, intense Asian competition and the overall rise of services.

If European GDP expands by a realistic 1.5 % annually in real terms, industry would need to grow by roughly 4–5 % per year on average to add six percentage points to its share within ten years. Achieving that pace seems impossible given the constraints of soaring energy costs, stringent environmental standards, fierce competition and persistent European dissonance.

Germany has pressed for the measures to be relaxed, targeting strategic sectors and ensuring proportionality. A mixed compromise? It’s only the beginning. The text still has to be negotiated and approved by the European Parliament and the European Council.

By contrast, the Nordic countries—Sweden, Denmark, Finland, and especially the Netherlands—are strong proponents of free trade. As net exporters, they oppose any form of protectionism, even a light‑touch version.

And then what? Suppose the Commission’s proposal is adopted unchanged. The system would likely become even less effective, because it would be easy to circumvent. The simplest workaround is to produce the goods on European soil—a practice already widespread. A Chinese firm can open a factory in Europe, and if a sufficient portion of the manufacturing occurs there, the product can be labelled “Made in Europe.”

The alternative is to rely on partner countries. In that scenario, components would be manufactured in China, assembled in Turkey or Morocco, and then exported to the EU. It is doubtful that the much‑vaunted, hoped‑for European re‑industrialisation will benefit significantly from such a scheme. Yet it is easy to see how production can be shifted to low‑cost jurisdictions.

One question: does Europe really exist beyond treaties and the inner‑circle commissions? Let’s listen to Eric Trappier, CEO of Dassault Aviation.

“What effective fighter jet has Europe produced? There isn’t one. The only one is the French one. At least we know how to build fighter jets in France. People will tell me, “We made the Eurofighter.” But of the four countries that developed the Eurofighter, three bought the F-35. That’s what decline looks like.”